Economics

3343: Course Project

Dr. Philip Rothman

Office: Brewster A-424

Phone: 328-6151

Email: rothmanp@ecu.edu

Due date/time: Thursday, May 9, 8am. A hard copy of the paper needs to be submitted upon your arrival

for the Final Exam; submission by e-mail will NOT be accepted; if you wish,

you may submit the paper before the due date/time.

I. Topical Focus

Your project will be based upon analysis of a

set of estimated regression models motivated by what is known as the Capital

Asset Pricing Model (CAPM). I have provided a Brief

Introduction to the CAPM and Factor Models, with an emphasis on some key

econometric issues; you are STRONGLY ENCOURAGED to

read through and ‘digest’ that material ASAP. The remainder of this document

assumes you indeed are sufficiently familiar/comfortable

with that material.

II. Data

Each student will use the following data to

estimate the CAPM and factor models:

1.

The excess return on the ‘market portfolio’ (![]() ) from the Fama

and French Data Library.

) from the Fama

and French Data Library.

2.

The ‘change in risk premium’ (![]() ) measure given by the difference between the yields on Baa and Aaa rated bonds.

) measure given by the difference between the yields on Baa and Aaa rated bonds.

3.

The ‘small minus big’ (![]() ) measure from the Fama

and French Data Library.

) measure from the Fama

and French Data Library.

4.

The ‘high minus low (![]() ) measure from the Fama

and French Data Library.

) measure from the Fama

and French Data Library.

Note: various combinations of the above data

will be used as the INDEPENDENT or EXPLANATORY variables in your estimated regression models. You can download

these data in an EViews workfile

by CLICKING HERE. The EViews variable names for these data are: ‘er_mkt’ for the excess return on the market portfolio; ‘crp’ for the change in risk premium; ‘smb’

for the ‘small minus big’ size premium measure; and ‘hml’

for the ‘high minus low’ size premium measure. Note that these are monthly data

and the sample period starts in July of 2001 and ends in December of 2012.

Each student has been assigned a different stock (a

‘security’ in the language of CAPM and factor models), such that each of you

will be using different data for the DEPENDENT variable in your regression

models. Each of these securities is a component of the S&P500 stock index.

To see which stock you have been assigned, CLICK HERE. The link associated with your

name will take you to a Yahoo Finance web

site at which you can download the historical data you will need. Once you are

at this site:

1. For the ‘Start Date,’ you should

enter ‘June 1, 2001’

2. For the ‘End Date,’ you should

enter ‘December 31, 2012’

3. You should indicate that you want

‘Monthly’ data

4. After you have specified these

parameters, scroll down and click on the ‘Download to Spreadsheet’ link. This

will allow you to download your download into a ‘Comma-Separated-Value’ (with

the extension ‘csv) file which can be opened with

Excel. CLICK HERE to see such a file with data on the ExxonMobil Corporation’s stock

price. For a student assigned ExxonMobil’s stock for this project, the data

series needed for the assignment would be in the last column under the heading

‘Adj Close’ (for ‘adjusted closing price,’ where the

price at the end of trading is adjusted for dividends and stock splits.

Below is an

explanation of how you need to transform such data for use in the project:

1. Delete all the columns from the initial

file except the first one (with the dates) and the last one (with the ‘Adj Close’) data. For an example, CLICK HERE; note that the initial CSV file

has been saved into an Excel file. Note: when you create an Excel file, make sure to save

it as an ‘Excel 97-2003 Workbook’ (i.e., with an ‘xls’

extension, not an ‘xlxs’ extension).

2. Next, arrange the data in

chronological order, i.e., oldest to newest. To do so, highlight all data cells

in the file, then left click, then click on Column

> Sort by ‘Date’, Sort On >

Values, ‘Sort,’ and then Order > ‘Oldest

to Newest. To see what you get after doing this, CLICK HERE.

3. Next, compute the month-to-month

growth rate in the ‘Adj Close’ measure. An easy way

to do this would be to copy the formula in cell ‘C3’ from THIS FILE, paste it in your file, and then

use it fill out the cells ‘C3-C140’ in your file. The variable name ‘r’ in cell

‘C1’ stands for the rate of return on the stock/security you’ve been assigned.

4. Next, copy the data for the

variable ‘rf’ (the ‘risk-free rate’ measure from the Fama

and French Data Library) from

column ‘D’ in THIS

FILE and past the

copied data into column ‘D’ in your file (starting in cell D3).

5. Next, for each row, subtract the

entry from the cell in column ‘D’ from the entry for the cell in column ‘C,’ as

done in THIS FILE. Note that this computes the

‘risk premium’ for the stock; the name in cell ‘E1,’ ‘er_r,’

is meant to indicate the excess return on the stock/security you’ve been

assigned computed using the rate of return on the stock/security.

6. Next, highlight cells ‘E1’ to

‘E140,’ right-click and then click on ‘Copy,’ then place the cursor on cell

‘E1,’ right-click and then click on ‘Paste Special’ and then under ‘Paste’

click on ‘Values’ and then ‘OK.’ Then delete columns ‘B ‘

through ‘D’; and also delete Row 2. Then replace the entries in Column

‘A’ with the Column ‘A’ from THIS FILE.

7. Finally, enter the data you have

computed for the stock’s excess return into EViews by

following these steps: (a) open THIS EViews WORKFILE

in EViews; (b) left-click File

> Import > Read Text-Lotus-Excel, then go to the folder where the

Excel file with your ‘er_r’ data is located and click

on the file to indicate to EViews that this is the

file you want to import (note: make sure the Excel file is NOT open in Excel);

(c) in the EViews window that opens, the ‘upper-left

data cell’ should be ‘B2’ and, in the ‘Names for series or Number if names in

file’ box, enter ‘1’ and then hit the ‘OK’ button. Now the series ‘er_r’ will also be in the file.

Now you have

data with which you can estimate equations (3), (6), (7), and (8), i.e.,

equations for the CAPM and the factors models discussed HERE.

III. Econometric Tasks

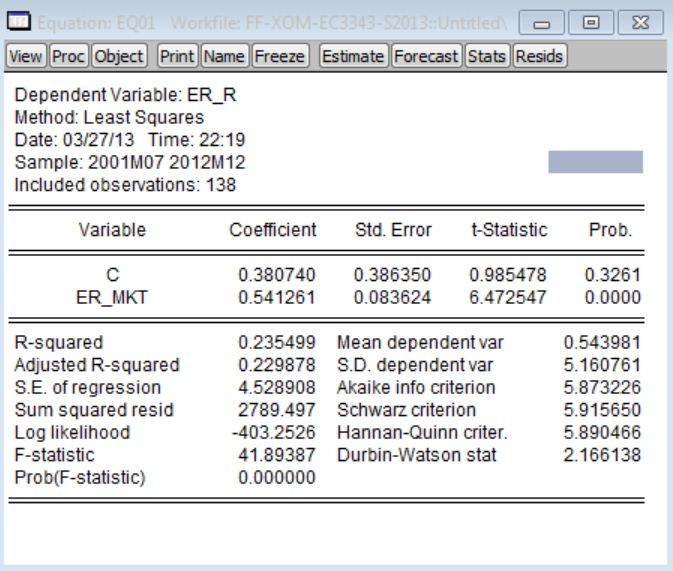

1. Estimate the CAPM equation (3) by

OLS. [You can do this in EViews as follows: (a) put the cursor on the command line

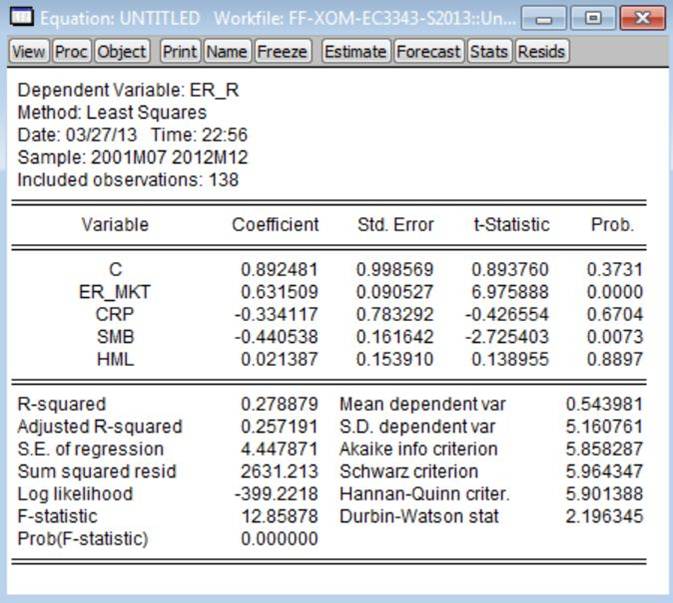

(top-left corner of screen); (b) type: ls er_r c er_mkt; (c) hit the ‘Enter’ key.] Refer to this as ‘Model 1.’ Using the Exon Mobil excess returns data

as the dependent variable, the estimated version of Model 1 is:

Note:

After this model has been, you should left-click on Name > OK; make sure to do this for all of the estimated models

for this project. The default name for the first estimated model stored in a workfile is ‘eq01’. You should also make sure to save your workfile.

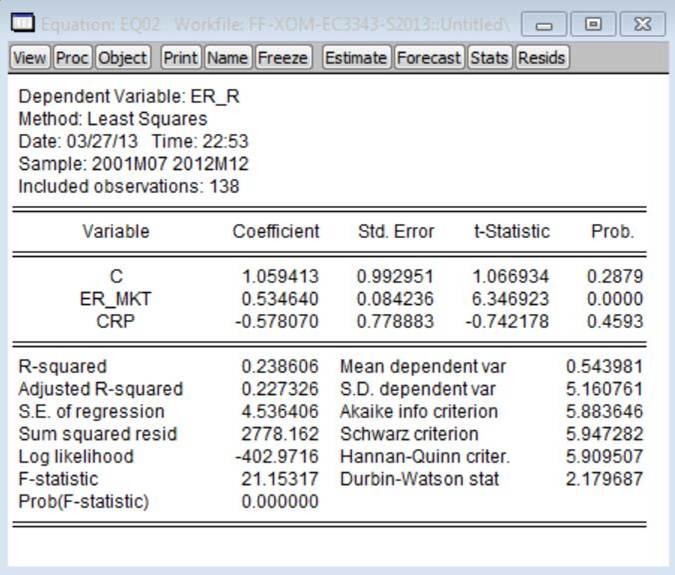

2. Estimate equation (6) by

OLS. [You can do this in EViews as

follows: (a) put the cursor on the command line (top-left corner of screen);

(b) type: ls er_r c er_mkt crp; (c) hit the ‘Enter’ key.] Refer to this as ‘Model 2.’

Using the Exon Mobil excess returns data as the dependent variable, the

estimated version of Model 2 is:

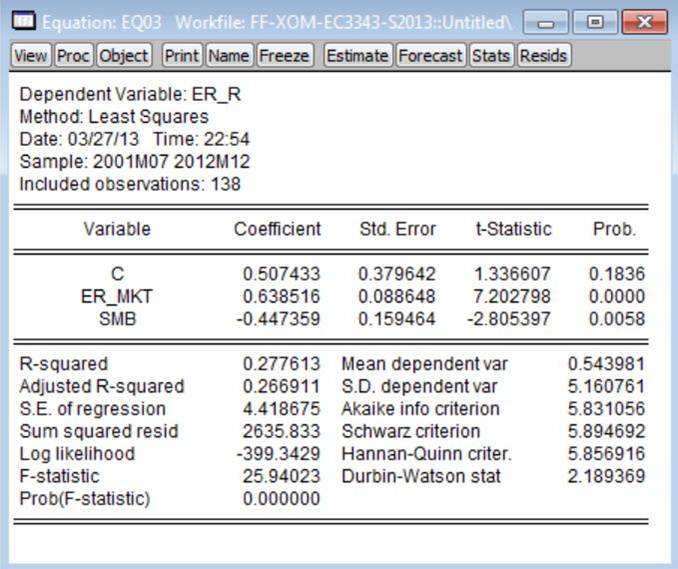

3. Estimate the model given by

adding the ‘small minus big’ variable to equation (3). [You can do this in EViews

as follows: (a) put the cursor on the command line (top-left corner of screen);

(b) type: ls er_r c er_mkt smb; (c) hit the ‘Enter’ key.] Refer to this as ‘Model 3.’ Using the Exon Mobil excess returns data

as the dependent variable, the estimated version of Model 3 is:

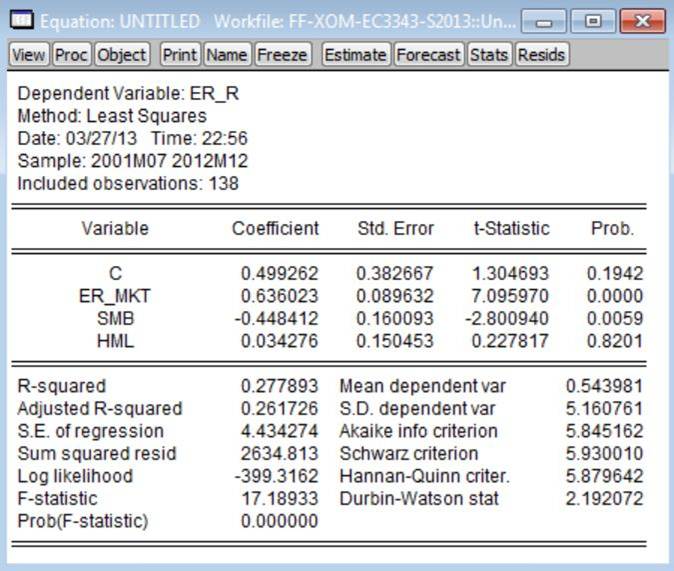

4. Estimate the model given by

adding the ‘high minus low’ variable to equation (3). [You can do this in EViews

as follows: (a) put the cursor on the command line (top-left corner of screen);

(b) type: ls er_r c er_mkt hml; (c) hit the ‘Enter’ key.] Refer to this as ‘Model 4.’ Using the Exon Mobil excess returns data

as the dependent variable, the estimated version of Model 4 is:

5. Estimate the three-factor model

given by equation (7). [You

can do this in EViews as follows: (a) put the cursor

on the command line (top-left corner of screen); (b) type: ls er_r c

er_mkt smb hml; (c) hit the ‘Enter’ key.] Refer to this as ‘Model 5.’

Using the Exon Mobil excess returns data as the dependent variable, the

estimated version of Model 5 is:

6. Estimate the four-factor combined

model given by equation (8). [You

can do this in EViews as follows: (a) put the cursor

on the command line (top-left corner of screen); (b) type: ls er_r c

er_mkt crp smb hml; (c) hit the ‘Enter’ key.] Refer to this as ‘Model 6.’ Using the Exon Mobil excess returns data

as the dependent variable, the estimated version of Model 6 is:

7. For each estimated model, test

the null hypothesis of no positive serial correlation against the alternative

hypothesis of positive serial correlation at the 5% significance level with the

Durbin-Watson test. Let’s see how this is done for the estimated version of

Model 1 above, for which the Durbin-Watson statistic = 2.166. Since a 1-sided

test is being run at the 5% significance level, the critical values ![]() and

and ![]() need to be obtained from Table 4 of the

‘Statistical Tables’ appendix. For all of the estimated regression models in

this project, the sample size is 138 (see ‘Included observations’ in the EVIews output). But note that the highest value of ‘N’

listed in Table 4 is 100. For the purposes of this project, we’ll use the

critical values associated for the N=100 case. For Model 1, K=1, so we use the

following critical values:

need to be obtained from Table 4 of the

‘Statistical Tables’ appendix. For all of the estimated regression models in

this project, the sample size is 138 (see ‘Included observations’ in the EVIews output). But note that the highest value of ‘N’

listed in Table 4 is 100. For the purposes of this project, we’ll use the

critical values associated for the N=100 case. For Model 1, K=1, so we use the

following critical values: ![]() and

and ![]() . Since DW = 2.166 > and

. Since DW = 2.166 > and ![]() , the decision rule for this test

implies that the null hypothesis is not rejected at the 5% significance level.

, the decision rule for this test

implies that the null hypothesis is not rejected at the 5% significance level.

8. For the estimated Models 1

through 6, run the hypothesis tests specified in items I-VI found on p. 3 of THIS FILE. Note that p-values for all but one of these null hypotheses (i.e., the

one for hypothesis test III) are provided in the standard regression output

produced by EViews. So, to “run” these tests after the

models have been estimated, there’s nothing to do other than to properly

interpret the associated p-values. To

run hypothesis test III, assume that, as in the EViews

examples highlighted above,

the opening ‘ls er_r’ is always followed by ‘c er_mkt’ (and other dependent variable names in Models 2-6), i.e., after

telling EViews to run an OLS regression with ‘er_r’ as the dependent variable, a constant is specified and then ‘er_mkt’ is listed as the first independent variable. Then, once the model has

been estimated, do the following: click on View

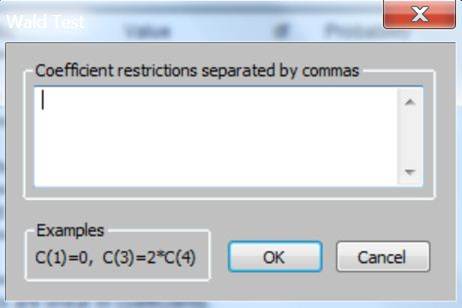

> Coefficient Tests > Wald – Coefficient Restrictions. Then this

window will open up:

In the window enter: ‘c(2)=1’, as in:

The ‘c’ refers to the an EViews variable that stores

the estimated coefficients; the ‘2’ tells EViews that the test is to be

run on second coefficient stored in ‘c’; the first coefficient stored in ‘c’ is the estimated constant term. Doing

this test for the estimated version of Model 1 using the excess returns data on

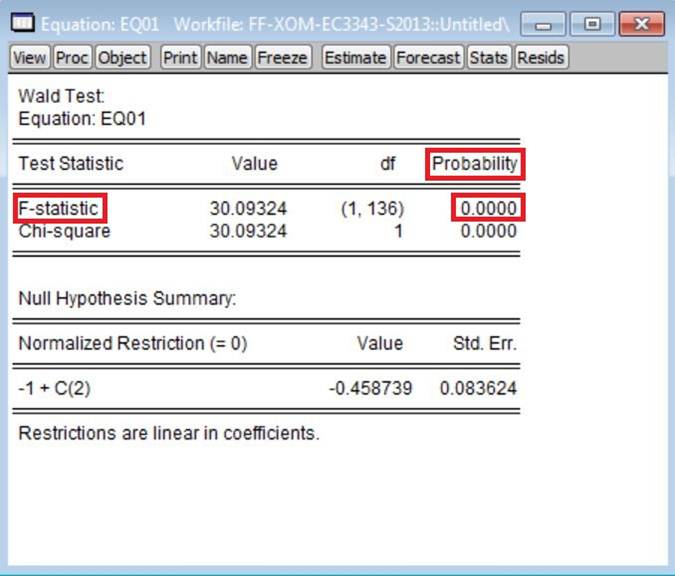

ExxonMobil’s stock leads to this (without the three red rectangles):

In the column labeled ‘Probability’ are p-values (for two approaches for

computing the p-value for this test).

You should use the p-value associated

with the ‘F-statistic’. Note: what EViews calls a

‘Wald Test’ is the ‘general F-test’

discussed in the appendix to Chp. 5 of the text.

Note: Suppose you’ve estimated Models 1 through 6 and stored the

estimated equations as ‘eq01’, ‘eq02’, …, ‘eq06’. You can

run hypothesis test III by first left-clicking on the particular equation name,

then clicking on View > Coefficient

Tests > Wald – Coefficient Restrictions, and running through the steps

given above.

9. For Models 5 and 6, test ![]() . Assuming these models have been

estimated with these exact commands, ‘ls er_r c er_mkt smb

hml’ and ‘ls er_r c er_mkt crp

smb hml’,

respectively, for Model 5 and Model 6. Assume Model 5 is stored in your workfile as

‘eq05’. Left-click on ‘eq05’ and then left-click on View > Coefficient Tests > Wald – Coefficient Restrictions to

get this window again:

. Assuming these models have been

estimated with these exact commands, ‘ls er_r c er_mkt smb

hml’ and ‘ls er_r c er_mkt crp

smb hml’,

respectively, for Model 5 and Model 6. Assume Model 5 is stored in your workfile as

‘eq05’. Left-click on ‘eq05’ and then left-click on View > Coefficient Tests > Wald – Coefficient Restrictions to

get this window again:

Then enter ‘c(3)=c(4)=0’ to test ![]() for Model 5. Next, Assume Model 6 is stored in your workfile as ‘eq06’. Left-click on ‘eq06’ and then

left-click on View > Coefficient Tests

> Wald – Coefficient Restrictions to get this window again:

for Model 5. Next, Assume Model 6 is stored in your workfile as ‘eq06’. Left-click on ‘eq06’ and then

left-click on View > Coefficient Tests

> Wald – Coefficient Restrictions to get this window again:

Then enter ‘c(4)=c(5)=0‘ to test ![]() for Model 6.

for Model 6.

10. For Model 6, test

![]() . Assume this model has been estimated with the command ‘ls er_r c

er_mkt crp smb hml’ and that the estimated model is stored as

‘eq06’. Left-click on

‘eq06’ and then left-click on View >

Coefficient Tests > Wald – Coefficient Restrictions to get this window

again:

. Assume this model has been estimated with the command ‘ls er_r c

er_mkt crp smb hml’ and that the estimated model is stored as

‘eq06’. Left-click on

‘eq06’ and then left-click on View >

Coefficient Tests > Wald – Coefficient Restrictions to get this window

again:

Then enter ‘c(3)=c(4)=c(5)=0‘ and click on ‘OK’ to test ![]() for Model 6.

for Model 6.

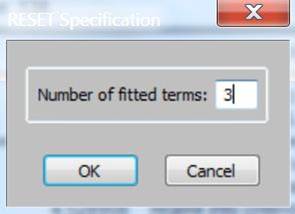

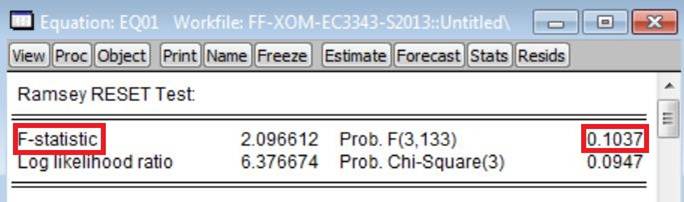

11. Run the RESET test for each model. Suppose you’ve estimated Models 1

through 6 and stored the estimated equations as ‘eq01’, ‘eq02’,

…, ‘eq06’. You can run the RESET test

by first left-clicking on the particular equation name, then clicking on View > Stability Tests > Ramsey RESET

Test, entering ‘3’ for the number of ‘fitted terms’ when this window pops

up:

and then clicking ‘OK’. Doing this for Model 1 estimated with the Exon

Mobil excess returns data as the dependent variable generates these results:

For your project, you should report the p-value associated with the ‘F-Statistic’ version of the RESET test.

12. Report your results for all of

the above in a table. If you click HERE,

you can download a WORD file with a table reporting such results for Models 1

through 6 estimated using the ExxonMobil excess returns stock data as the

dependent variable. You can use this WORD file as a template.

13. Run Bias Checks for each of the explanatory variables in Models 2

through 6, examine the effect (on the slope coefficients for other independent

variables) of dropping the variable from the model; discussion of this analysis

should be included in your paper. These are the particular bias checks you should examine:

a. Dropping ‘er_mkt’

from Model 2.

b. Dropping ‘er_mkt’

from Model 3.

c. Dropping ‘er_mkt’

from Model 4.

d. Dropping ‘er_mkt’

from Model 5.

e. Dropping ‘er_mkt’

from Model 6.

f.

Dropping ‘crp’ from Model 2.

g. Dropping ‘crp’

from Model 6.

h. Dropping ‘smb’

from Model 3.

i.

Dropping ‘smb’ from Model 5.

j.

Dropping ‘smb’ from Model 6.

k. Dropping ‘hml’

from Model 4.

l.

Dropping ‘hml’ from Model 5.

m. Dropping ‘hml’

from Model 6.

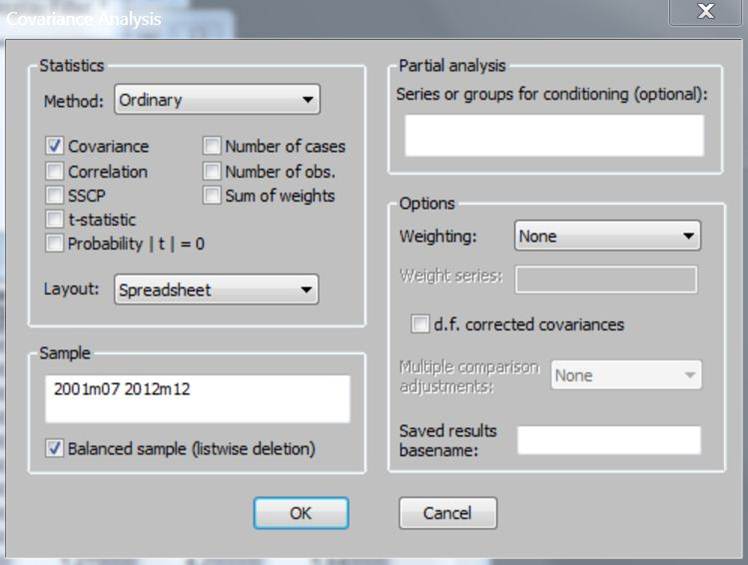

To

help analyze these results, it will be useful to have information on the

estimated correlations between the different independent variables. To produce

this information, first create an EViews ‘group’ with

the variables ‘er_mkt’, ‘crp’,

‘smb’, and ‘hml’. Then

click View > Covariance Analysis.

When this window opens up:

uncheck ‘Covariance’, check ‘Correlation’, on the ‘Layout’

table click ‘Single table’, and then click on ‘OK’. This window will then pop

up:

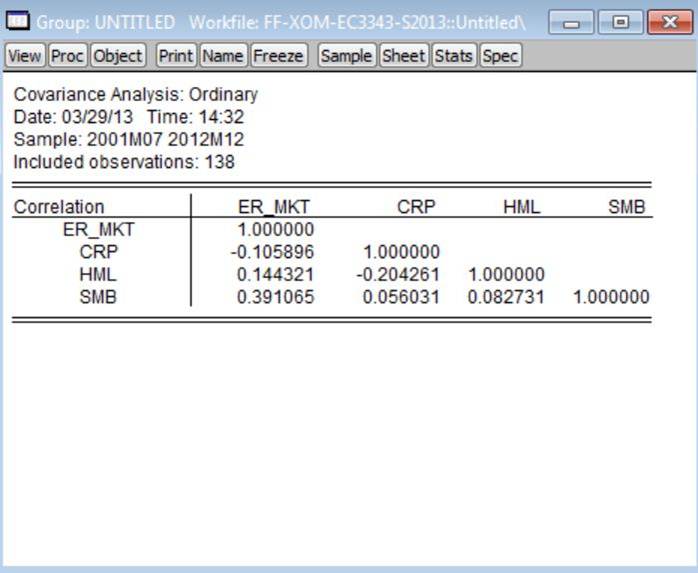

From

this table, we see the following sample correlation coefficients: (a) corr(er_mkt, crp) = -0.11; (b) corr(er_mkt, hml)

=0.14; (c) corr(er_mkt, smb) = 0.39; (d) corr(crp, hml) = -0.20; (e) corr(crp, smb)

=0.06; and (f) corr(hml, smb) = 0.08.

14. Based upon the results you obtain

and the underlying economic theory, determine which of the models you have

estimated is the ‘best’ model. In making this judgment, you should consider at

least the following criteria (which you might want to consider, along with

steps above, as part of the ‘rubric’ for this project):

a)

t-Test:

Is the variable’s estimated coefficient significant (at conventional

significance levels) in the expected direction?

b)

F-Test:

Is the variable’s estimated coefficient jointly (i.e., along with the

other estimated slope coefficients in the equation) significantly different

from zero (at conventional significance levels)?

c)

R-Bar-Squared: Does the overall fit of the

equation (adjusted for degrees of freedom) improve when the variable is added

to the model?

d)

Bias Check:

Do other variables’ coefficients change significantly when the variable

is added/deleted from the equation?

e) RESET Test: Does the RESET Test fail

to reject the null of no specification error when the variable is added to the

equation?

IV. Paper

Write a

paper describing what you have done and analyzing your results. Some specifics:

·

Your paper

should have at least three sections: ‘Section 1: Introduction’; ‘Section 2:

Analysis’; and ‘Section 3: Conclusions’; make sure your paper has a title page

and that, if your paper is not presented in a special report-type folder, all the pages are

stapled together (if they

are not stapled, your paper will not be accepted).

·

As part of

your analysis, it would be interesting to discuss the values of ![]() relative to 1. For example,

for all of the estimated Models 1 through 6 using the ExxonMobil excess returns

data at the dependent variable, of

relative to 1. For example,

for all of the estimated Models 1 through 6 using the ExxonMobil excess returns

data at the dependent variable, of ![]() < 1, implying that the

returns for this stock are less volatile than returns on the overall market.

Does this make sense? It’s a ‘BLUE CHIP’

stock that’s one of the components of the DOW

JONES INDUSTRIAL AVERAGE that has a LONG

RECORD OF PAYING DIVIDENDS. These features of ExxonMobil’s stock indeed

suggest that it’s a relatively less risky investment; note that ‘less risky’

does not mean ‘not risky.’ So, the value of

< 1, implying that the

returns for this stock are less volatile than returns on the overall market.

Does this make sense? It’s a ‘BLUE CHIP’

stock that’s one of the components of the DOW

JONES INDUSTRIAL AVERAGE that has a LONG

RECORD OF PAYING DIVIDENDS. These features of ExxonMobil’s stock indeed

suggest that it’s a relatively less risky investment; note that ‘less risky’

does not mean ‘not risky.’ So, the value of ![]() relative to 1 for this

stock makes sense.

relative to 1 for this

stock makes sense.

·

It would also be interesting to compare the values

you obtain for ![]() relative to those reported

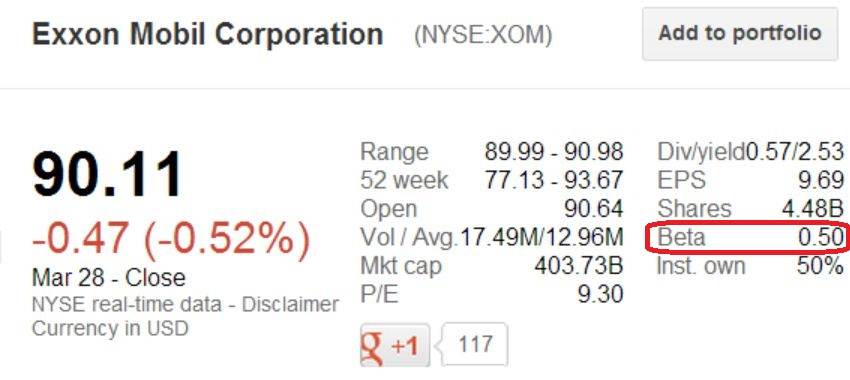

by various financial web sites. For example, this is what Google Finance

reports:

relative to those reported

by various financial web sites. For example, this is what Google Finance

reports:

this is

what Reuters reports:

and this

is what Yahoo Finance reports:

The

‘beta’ values from Google Finance and Reuters are close to the

![]() for Models 1, 2, & 4. The ‘beta’ value from Yahoo Finance is

roughly halfway between the

for Models 1, 2, & 4. The ‘beta’ value from Yahoo Finance is

roughly halfway between the ![]() for Models 1, 2, & 4, and those in Models 3 & 5. What might

account for these differences and similarities? This question is discussed HERE.

for Models 1, 2, & 4, and those in Models 3 & 5. What might

account for these differences and similarities? This question is discussed HERE.

·

You should

also include (and discuss) scatter plots between the excess returns for the

stock you have been assigned and the following variables: (i)

the excess returns on the market portfolio; (ii) the change in risk premium

measure, i.e., the variables ‘crp’; (iii) the size

premium measure, i.e., the variable ‘smb’; and (iv)

the value premium measure, i.e., the variable ‘hml’.

[Note that this means a total of four scatter plots; you can find an

explanation of how to combine these four scatter plots into one graph HERE]. Recall the distinction between

‘unconditional’ and ‘conditional’ correlations from the warm-up HW assignment. HERE is a WORD file with the

scatterplots using the ExxonMobil excess returns data.

·

To help you

refer to the population regression models to be estimated for the paper, HERE is a WORD file with these models

written using the WORD equation editor; you may copy & paste these as you

wish for your paper.

·

Remember:

(a) to properly reference all sources you use; and (b) NOT TO PLAGIARIZE.

Last updated: April 26, 2013. Link to: Econometrics Home Page.